This regularly scheduled column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at [email protected].

Question: How has the Arlington single-family home market performed in the first half of 2026?

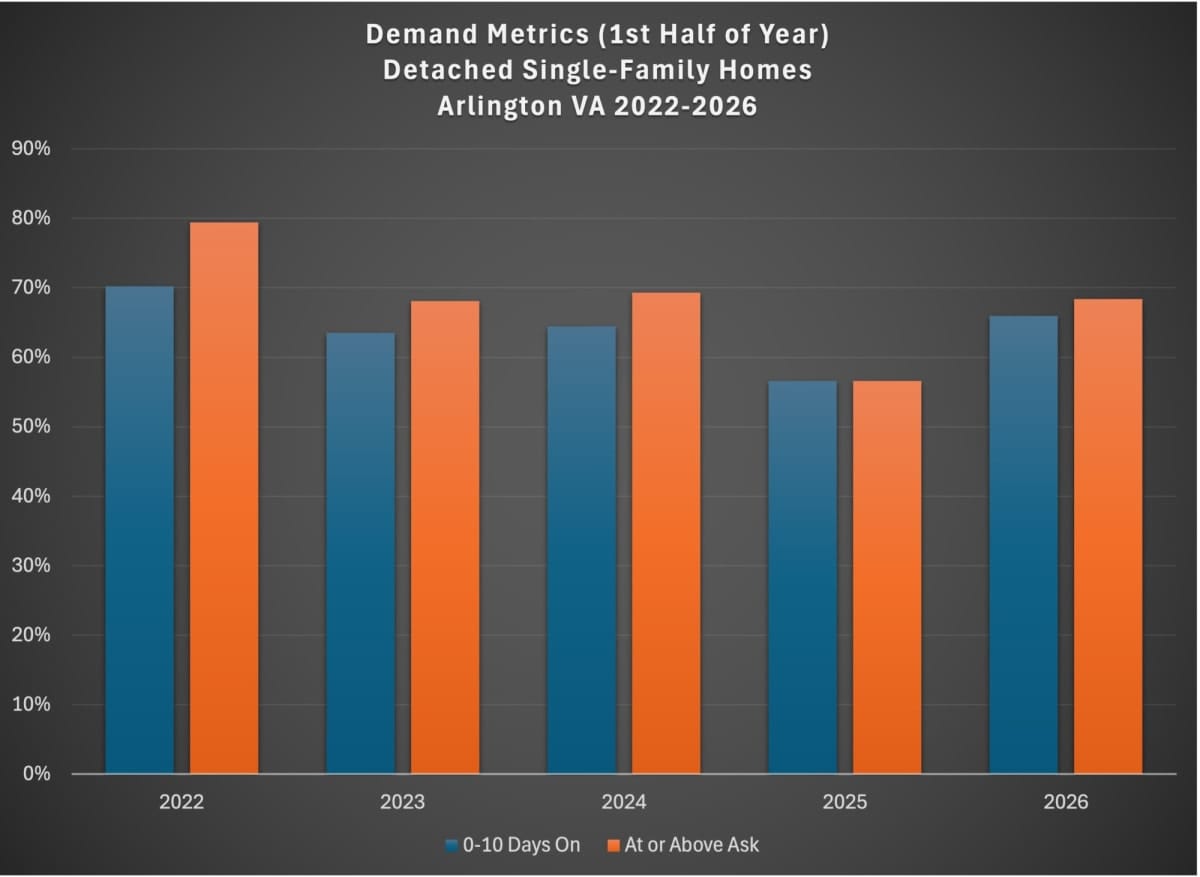

Answer: Arlington’s single-family detached (SFD) market got busier and more competitive in the first half of 2026, yet prices increased at their slowest pace since 2023.

More Competition, Modest Appreciation (Resale Market)

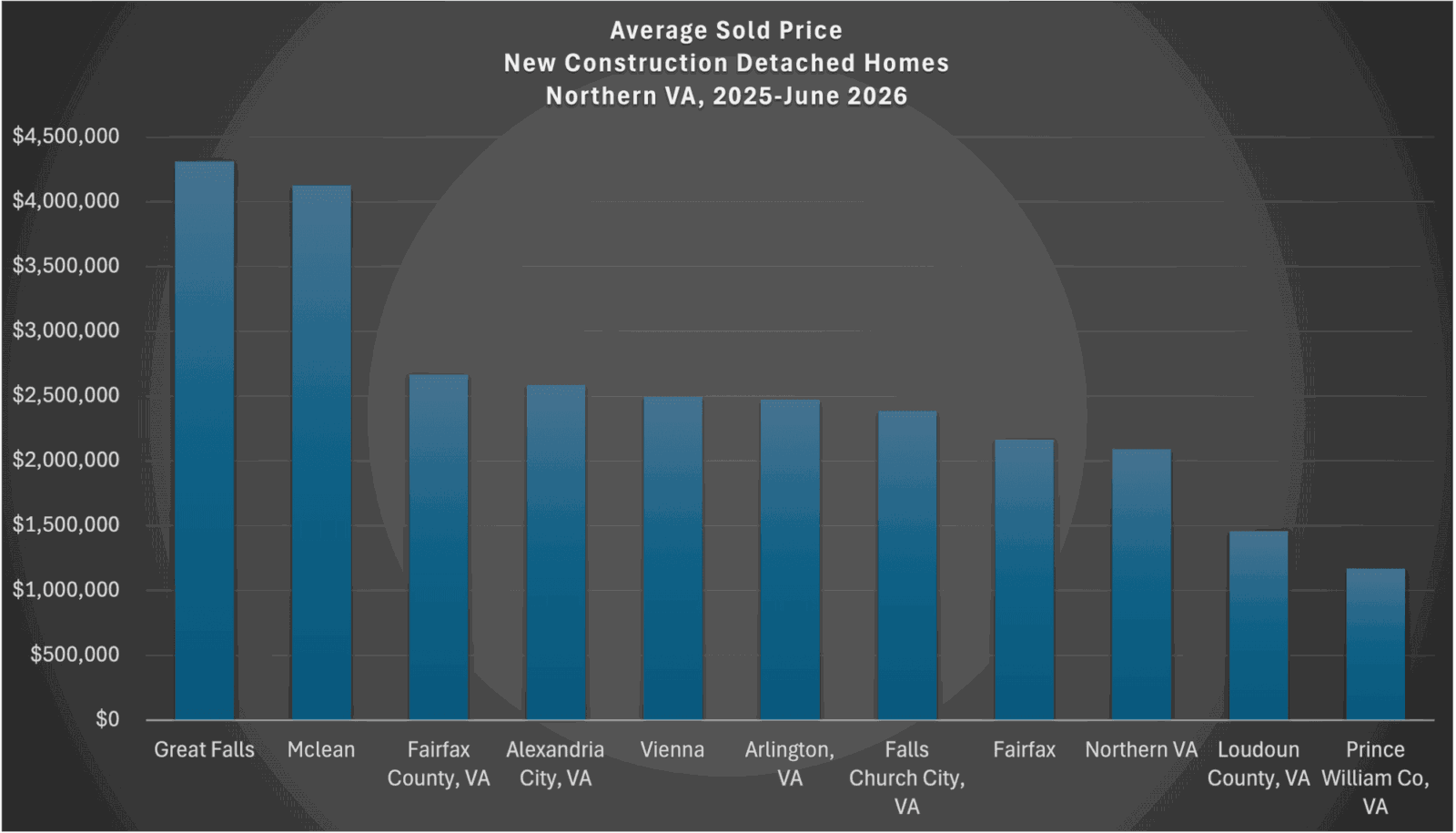

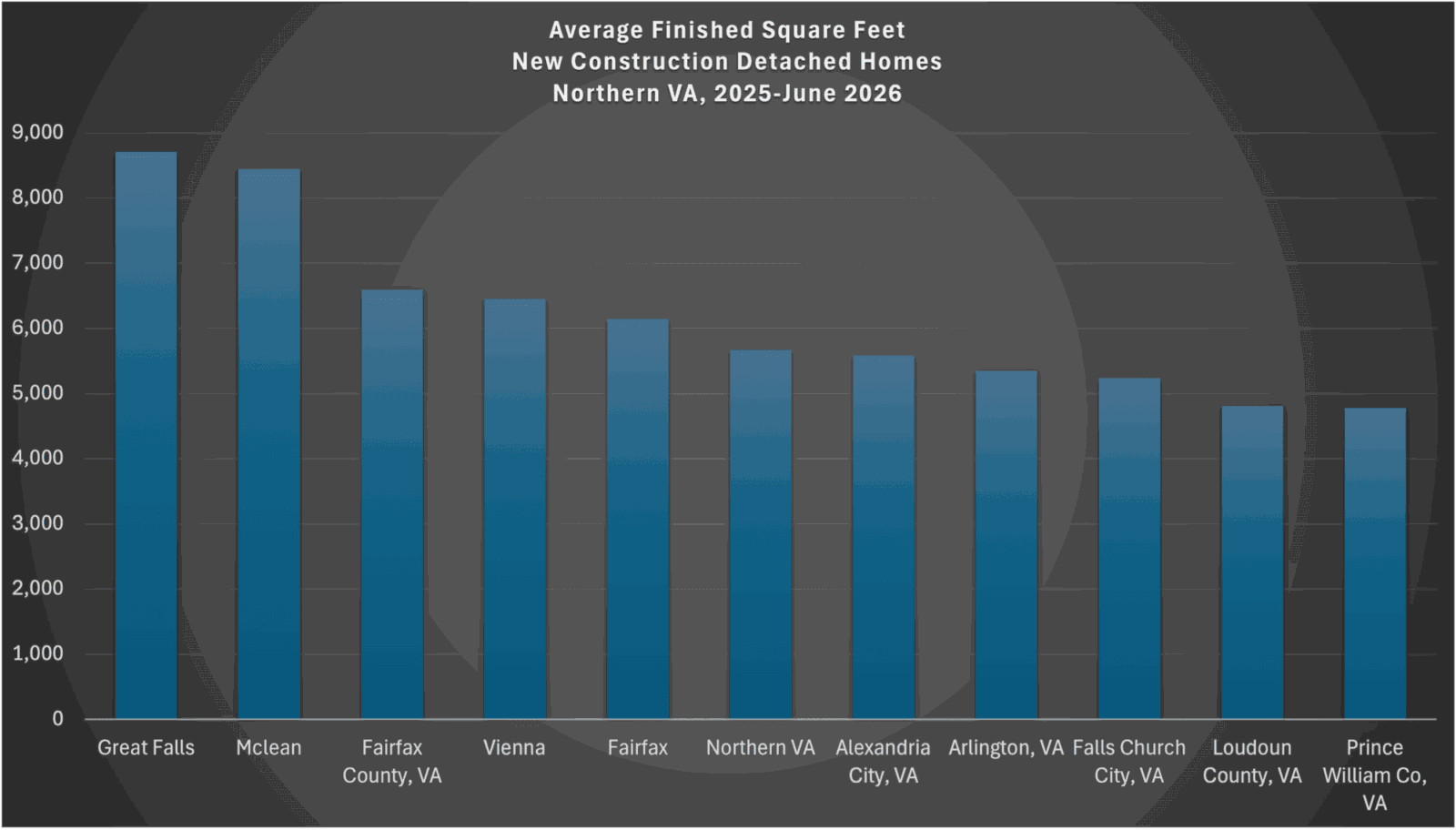

Note: this data is for resales of single-family detached (SFD) homes; I have a separate analysis of the new construction market further down.

- The average and median price increased 3.5% and 1.9%, respectively

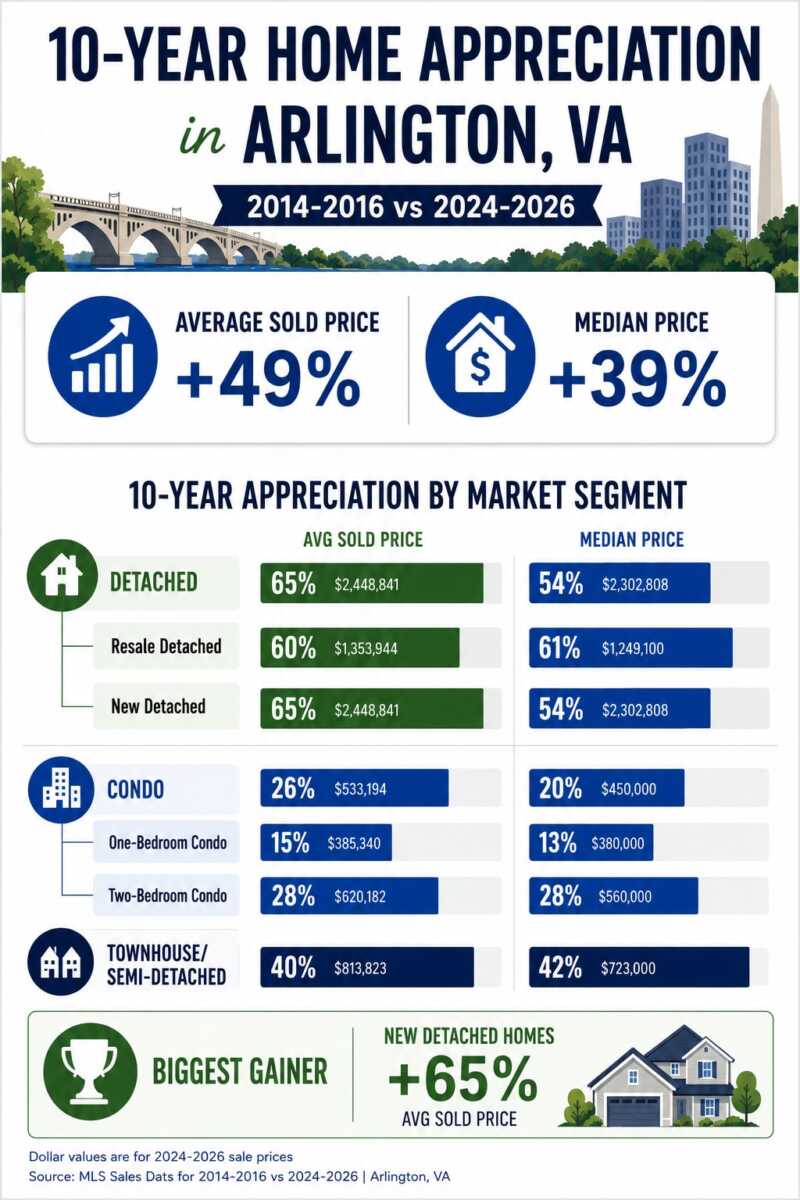

- Over the past five years, the average and median price increased 13.9% and 11.1%, respectively

- The average and median price of a home increased to $1.44M and $1.299M, respectively

- Demand and competition rose to the highest levels since 2022, with 66% of homes selling within the first ten days on market and 68% of homes selling at or above the original asking price

- The average buyer paid 1.3% more than the original asking price, compared to 2025 when the average buyer paid 0.3% less than the original asking price

- Buyers of homes that went under contract within the first week on market paid an average of 4.7% over the asking price

Dig Deeper: Performance Varied by Size, Price Point

The appreciation gap between the average price (3.5%) and median price (1.9%) matters. The average is more sensitive to expensive sales. In 2026, 15.7% of closed resales sold for $2M or more, up from 12.7% in 2025. At the other end of the market, only 21.7% sold below $1M, down from 24.4%. That shift toward higher-priced homes helped lift the average faster than the median.

Average and median prices are useful, but neither tells us whether gains were shared evenly across the market. To test that, I divided the closed resale market into four sold-price quartiles for each year. Each quartile represents one-fourth of that year’s sales, from the least expensive 25% to the most expensive 25%. (more…)