This regularly scheduled column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: Does the cost of renting a home in Arlington increase at a similar rate as the cost of buying a home in Arlington?

Answer: The cost of renting and buying a detached home increases at a similar rate, but the cost of renting a condo has outpaced the cost of buying a condo.

Condo Rents Rising Faster than Condo Prices

Since 2020, the cost of renting a detached home in Arlington increased at a similar rate as the cost of buying a detached home; 26% and 28%, respectively.

However, the cost of renting a condo increased significantly faster than the cost of buying a condo; 21% and 6%, respectively.

Sale Price to Rental Rate Multiple Shifts with Interest Rates

The table below shows the average price and $/SF of buying a detached home or condo relative to the average annual rent for a detached home or condo, in Arlington. Higher multiples show that buying is becoming more expensive relative to renting.

Takeaway: Condo buyers are more rate sensitive than detached home buyers and are more likely to rent (higher rental demand = strong condo rent appreciation) than buy (weakened purchase demand = low condo value appreciation) when interest rates increase. Notice how quickly the sale price to rental rate multiple drops from 2020/2021 to 2022/2023 (rates skyrocketed spring/summer 2022). (more…)

This regularly scheduled column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: How has the local real estate market performed so far this year?

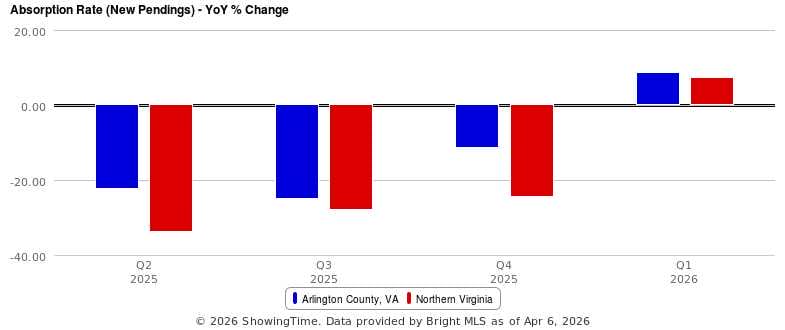

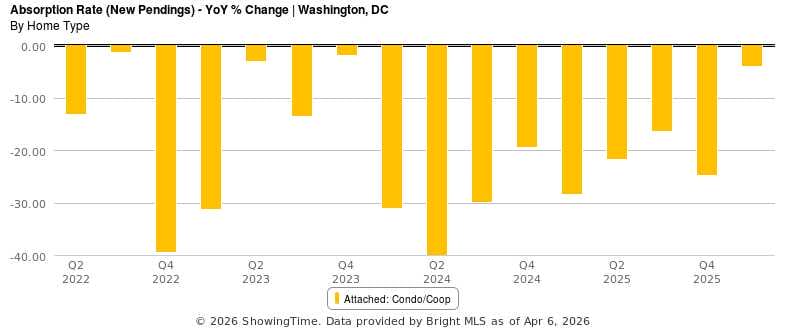

Northern VA, Arlington, and Washington DC Absorption Trends (demand)

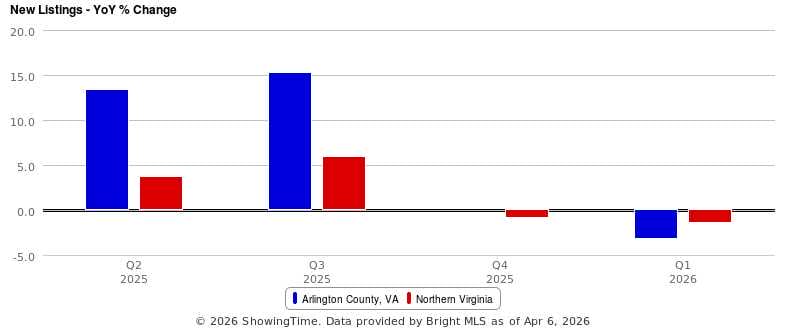

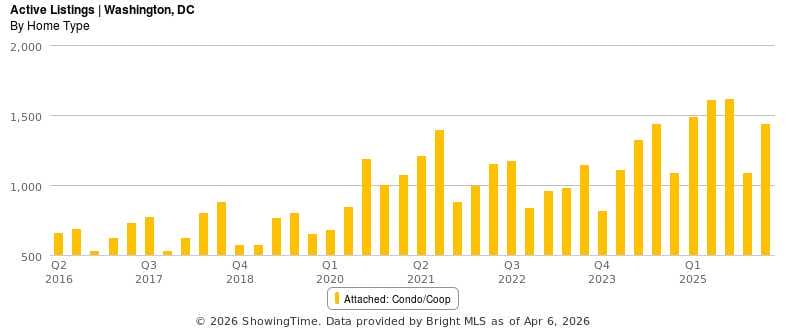

Northern VA, Arlington, and Washington DC Inventory Trends (supply)

Washington DC List Price Trends (market values)

Northern VA & Arlington Inventory is Being Absorbed Faster

After four straight quarters of double-digit decreases in year-over-year absorption, the Northern VA and Arlington markets saw a ~8% increase in absorption rate.

What this means: Demand increased in Q1

Northern VA & Arlington New Listing Volume is Declining

After a promising trend of six straight quarters of year-over-year increases in the number of homes listed for sale in Northern VA, new listing activity fell by ~1% each of the previous two quarters.

What this means: Sellers have less competition, buyers have fewer choices

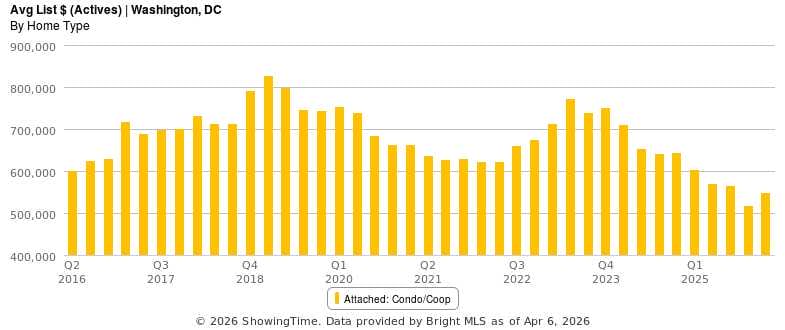

Washington DC Condo Absorption is Plummeting

The absorption rate for DC condos has declined year-over-year for 16 quarters straight and 23 out of the past 26 quarters.

What this means: It is difficult to find buyers for DC condos

Washington DC Condo Inventory Declined Slightly

Total inventory declined by 3.4% year-over-year, the first quarterly drop since Q4 2023. Still, there were great than 2x more condos for sale in DC in Q1 2026 than Q1 2020

What this means: Motivated sellers must compete aggressively with each other for buyers

Washington DC Condos Keep Getting Cheaper

The average price of a DC condo listed for sale is 9.4% less than it was in Q1 2025 and ~9% less than it was ten years ago.

What this means: Even lowering the price won’t guarantee a buyer

If you’d like to discuss buying, selling, investing, or renting, don’t hesitate to reach out to me at [email protected].

We have access to the most pre and off-market listings across the DMV of any brokerage and are happy to share what’s available with anybody who asks.

Below are some of our team’s pre/off-market listings, details and additional listings available by request:

Westover – 4BR/2BA/2,000sqft – Detached Single Family (2000) – 23rd St N Arlington VA 22205

Green Valley – 5BR/4.5BA/3,000sqft – Detached Single Family (2020) – 24th St S Arlington VA 22206

Ballston – 4BR/3.5BA/2,400sqft – Townhouse (2008) – N George Mason Dr Arlington VA 22203

Ballston – 4BR/3.5BA+office/4,000 sqft – Four Townhouses (2026/2027) – 11th St N Arlington VA 22201

Rosslyn – 2BR/2BA/1,800sqft – Condo (2021) – 1781 N Pierce St Arlington VA 22209

Williamsburg – 6BR/5.5BA/5,500 sqft – Detached Single Family (2026) – 27th St N Arlington VA 22207

Yorktown – 6BR/6.5BA/6,000+ sqft – Detached Single Family (2026) – N Greencastle St Arlington VA 22207

Eli and his team believe that your real estate needs should be managed by advisors, not salespeople. Their mission is to guide, educate, and advocate for their clients through real advice, hands-on support, and personalized service.

This regularly scheduled sponsored column is written by Carolanne Korolowicz, Arlington-based Realtor and Arlington resident. If you would like to work with Carolanne in Northern Virginia and the greater D.C. Metro area, you can reach her directly at[email protected].

As Spring peaks, Northern Virginia features flowering azaleas, dogwood canopies, and pesky dandelions. Manicured lawns flaunt along neighborhood streets, and Mother Nature continues to outshine in parks, trails and the spaces in between.

Home to a plethora of flora and fauna, Virginia has a long history of impressive grounds. The “Mother of Presidents” could also tack on, “and Their Gardens.” Many of these impressive natural displays are publicly accessible, but many of these gardens rooted in history are found at private residences. The Garden Club of Virginia (GCV) devotes an entire year of planning and preparation for their signature event, Historic Garden Week, to give the public a peek behind the fence.

Photo Courtesy of The Garden Club of Virginia

The annual event is divided by region and tours span over the week (April 18–25). Northern Virginia kicks off in Old Town Alexandria this Saturday from 10:00 AM–4:00 PM. Tickets include tours of five rowhomes’ grounds, admission to Mount Vernon Estate and Gardens, and complimentary refreshments. (more…)

This regularly scheduled column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: Can you explain the latest news about partnerships between brokerages and websites like Redfin and Zillow for pre-market inventory?

Answer:

The fight over listings has shifted from theory to reality. Major brokerages, portals, and platforms are actively reshaping where listings appear, what data is shared, and who controls it. For buyers and sellers, the biggest risk isn’t who wins, it’s what gets lost if the market becomes fragmented.

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: How many different real estate agents are doing business in Arlington?

Answer: There were 2,317 real estate transactions in Arlington last year, totaling $2.136B in sales volume, increases of 6% and 8.4%, respectively, over 2024.

There were 2,116 licensed real estate agents involved in at least one sale in Arlington in 2025, compared to 2,058 in 2024. Each transaction usually includes two real estate agents – one representing the buyer and another representing the seller. (more…)

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: I am weighing the financial pros and cons of where to live in the DMV. How does the cost of homeowners insurance vary between Virginia, Washington DC, and Maryland?

Answer: Homeowners insurance has gotten more expensive and guidelines stricter as claims have risen. For buyers choosing between buying a home in Virginia, Washington DC, or Maryland the difference in homeowners insurance costs is worth considering.

I interviewed my go-to insurance provider, Seth Kutner, with ACO Insurance about the differences he sees providing homeowners insurance across the DMV. If you want to reach Seth to discuss your policies or ask questions, you can reach him at [email protected]. (more…)

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: Where do you see single family home architecture evolving over the coming 5+ years?

Answers: Predicting the next evolution of single-family home architecture requires a level of architectural expertise I do not have, so I asked the team at Lee Design Studio (Architecture, Design, Planning services based in Falls Church) for their input. I highly recommend Matt and his talented team of architects and designers, they can be reached at [email protected]

This regularly scheduled sponsored column is written by Carolanne Korolowicz, Arlington-based Realtor and Arlington resident. If you would like to work with Carolanne in Northern Virginia and the greater D.C. Metro area, you can reach her directly at[email protected].

For close to a century, the Arlington County Public Library system has been a robust resource for the community. With eight full-service locations, over 84,000 active patrons take advantage of the over two-million item collection, filled with both physical and digital materials. One of the promises of the Arlington Public Library is to provide a “third space” for innovation, conversation and community. With 5,000+ programs and events, Arlingtonians from infancy to retirement have a welcoming space to explore. From storytimes, The Shop, book clubs, and informative First-Time Homebuyer Workshops (shameless plug), no resident’s special interest is left behind.

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Arlington Assessments Up 3.2%, Tax Rate Up Too

In January, Arlington announced that residential property tax assessments increased by an average of 3.2%, higher than the ~1% increase in market values that I calculated for 2025. Last year’s 3.7% increase came in about half as high as the increase in market values I calculated for 2024, so Arlington had some catching up to do.

Arlington will increase the tax rate by 1.5 cents per $100 to $1.048 per $100, which comes out to a tax bill of 1.048% of your assessed value. (more…)

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Question: How did Arlington’s condo market perform in 2025?

The Headline: The Arlington condo market lost value in 2025 (down 4.9%), after surging in 2024 (up 10.7%). The overall Arlington market was up by just over 1%, on an average price basis.

Bucking, and Maintaining, the Trend

Arlington’s condo market is historically stable and predictable, but the past two years brought about an unusual period of volatility. Despite recent ups and downs, the long-term trend of 1-2% annualized growth has been maintained – over the past five years, the average sold price is up 7.3% and the average $/SF is up 4.8%. (more…)

This regularly scheduled sponsored column is written by Carolanne Korolowicz, Arlington-based Realtor and Arlington resident. If you would like to work with Carolanne in Northern Virginia and the greater D.C. Metro area, you can reach her directly at[email protected].

As the snow steadily fell, the temperature continued to plummet, and the ice encased the ground, I couldn’t help but dream of warmer days. Curled up on my couch, I escaped by scrolling Zillow and envisioning myself on a rocking chair with a water view. Deciphering my future vacation home, I thought the following, “Cancun is too distant, Florida’s weather is too unpredictable, and Rehoboth is too crowded…leaving the only option; Colonial Beach, Virginia.”

Though my previous statement is mostly in jest, Colonial Beach is honestly one of the area’s best kept secrets. Located just 85 miles from Arlington, the river town is low-key enough for a day trip and activity-filled enough for a long weekend. My parents recently purchased their get-away just steps from the Potomac River (the body of water that the beach is off of). They have found it to be a reprieve from city-life, a fantastic place to host all ages, and home to a great community of locals, part-timers, retirees and business owners.

This regularly scheduled sponsored column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. If you would like to work with Eli and his team in Northern Virginia and the greater D.C. Metro area, you can reach him directly at[email protected].

Questions: What design trends are you seeing in the residential market?

Answer: Every year our marketing department does a deep dive into home design trends that multiple local and national design experts say to look for each year. Some of these trends last just a year or two, others take hold for a decade. Often, these trends reintroduce styles from decades ago, with small tweaks.

You can click this link to browse the full 2026 Design Trends e-booklet from RLAH Real Estate. I’ve pulled out a few highlights and personal favorites below…

Color of the Year

Pantone: Cloud Dancer (11-4201). An “airy, ethereal white that embodies tranquility and gentle balance in a fast-moving world”.

Benjamin Moore: Silhouette (AF-655). A “rich and expressive hue” that blends burnished umber with subtle charcoal undertones.

Behr: Hidden Gem (N430-6A). A “moody jade infused with smoky depth” that feels both grounding and energized.

Sherwin Williams: Universal Khaki (SW 6150). A modern classic enriched with a soft yellow undertone, bringing warmth and ease to any space